You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

What I learned from 100 days of rejection.

- Thread starter Jones

- Start date

Thank you Jones.

Here's the authors blog and the list of rejection desensitisation exercises he completed in the 100 days.

When developing his exercises he insisted that they fit these criteria:

"Three criteria I set for myself: 1. Ethical (no lying or marriage-undermining) 2. Legal 3. Doesn't defy the law of physics."

He has links to the video's that he did for each of the rejection desensitisation exercises in the list.

www.rejectiontherapy.com

www.rejectiontherapy.com

When developing his exercises he insisted that they fit these criteria:

"Three criteria I set for myself: 1. Ethical (no lying or marriage-undermining) 2. Legal 3. Doesn't defy the law of physics."

He has links to the video's that he did for each of the rejection desensitisation exercises in the list.

100 Days of Rejection — Rejection Therapy

www.rejectiontherapy.com

Breo

The Living Force

What a good and funny way to put a magnifying glass on the topic of rejection. Really timely for me to pay attention as I lately try to observe what I tend to run away from but could not get hold of and phrase it. Its also another example of how a younger and immature self can destructively

run the show and needs to be educated or get out of the way to grow up.

Thanks Jones for posting!

run the show and needs to be educated or get out of the way to grow up.

Thanks Jones for posting!

What is most interesting is something we have discussed about many aspects of personality: that you can inoculate yourself against your triggers by deliberately exposing yourself to them! And, once the "triggering" stops being so automatic and powerful, your brain starts to come back online and you can actually work through the issues.

It's a really interesting experiment for sure. Each trial is low cost to the performer but each investment produces information he can use to improve his pitch and ability to get to yes. It's a good example of an endeavor having a "convex" or Antifragile nature (in that it benefits from repetition and increased uncertainty) as Nassim Taleb would say. The link below is about research and scientific advancement, but I would argue that it applies to Jia Jiang's experiment like a hand fits a glove.

SEVEN RULES OF ANTIFRAGILITY (CONVEXITY) IN RESEARCH

Next I outline the rules. In parentheses are fancier words that link the idea to option theory.

1) Convexity is easier to attain than knowledge (in the technical jargon, the "long-gamma" property): As we saw in Figure 2, under some level of uncertainty, we benefit more from improving the payoff function than from knowledge about what exactly we are looking for. Convexity can be increased by lowering costs per unit of trial (to improve the downside). (To me this resonates strongly with the idea that it is worse to introspect or theorize about an issue you face, and that it is better to put yourself out there and expose yourself to shocks and stressors to acquire much less ambiguous information about what NOT to do, which Tabel calls via negativa).

2) A "1/N" strategy is almost always best with convex strategies (the dispersion property): following point (1) and reducing the costs per attempt, compensate by multiplying the number of trials and allocating 1/N of the potential investment across N investments, and make N as large as possible. This allows us to minimize the probability of missing rather than maximize profits should one have a win, as the latter teleological strategy lowers the probability of a win. A large exposure to a single trial has lower expected return than a portfolio of small trials. (Each trial Jia did improved his chances in the next).

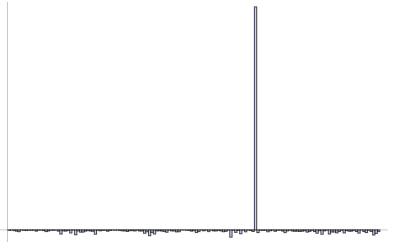

Further, research payoffs have "fat tails", with results in the "tails" of the distribution dominating the properties; the bulk of the gains come from the rare event, "Black Swan": 1 in 1000 trials can lead to 50% of the total contributions—similar to size of companies (50% of capitalization often comes from 1 in 1000 companies), bestsellers (think Harry Potter), or wealth. And critically we don't know the winner ahead of time.

Figure 3-Fat Tails: Small Probability, High Impact Payoffs: The horizontal line can be the payoff over time, or cross-sectional over many simultaneous trials.

3) Serial optionality (the cliquet property). A rigid business plan gets one locked into a preset invariant policy, like a highway without exits —hence devoid of optionality. One needs the ability to change opportunistically and "reset" the option for a new option, by ratcheting up, and getting locked up in a higher state. To translate into practical terms, plans need to 1) stay flexible with frequent ways out, and, counter to intuition 2) be very short term, in order to properly capture the long term. Mathematically, five sequential one-year options are vastly more valuable than a single five-year option.

This explains why matters such as strategic planning have never born fruit in empirical reality: planning has a side effect to restrict optionality. It also explains why top-down centralized decisions tend to fail.

4) Nonnarrative Research (the optionality property). Technologists in California "harvesting Black Swans" tend to invest with agents rather than plans and narratives that look good on paper, and agents who know how to use the option by opportunistically switching and ratcheting up —typically people try six or seven technological ventures before getting to destination. Note the failure in "strategic planning" to compete with convexity. (This means reject a top-down approach to development, because it falsely implies that you have everything figured out whereas you usually do not).

5) Theory is born from (convex) practice more often than the reverse (the nonteleological property). Textbooks tend to show technology flowing from science, when it is more often the opposite case, dubbed the "lecturing birds on how to fly" effect v vi. In such developments as the industrial revolution (and more generally outside linear domains such as physics), there is very little historical evidence for the contribution of fundamental research compared to that of tinkering by hobbyists. vii Figure 2 shows, more technically how in a random process characterized by "skills" and "luck", and some opacity, antifragility —the convexity bias— can be shown to severely outperform "skills". And convexity is missed in histories of technologies, replaced with ex post narratives. (Knowledge protects).

6) Premium for simplicity (the less-is-more property). It took at least five millennia between the invention of the wheel and the innovation of putting wheels under suitcases. It is sometimes the simplest technologies that are ignored. In practice there is no premium for complexification; in academia there is. Looking for rationalizations, narratives and theories invites for complexity. In an opaque operation to figure out ex ante what knowledge is required to navigate is impossible.

7) Better cataloguing of negative results (the via negativa property). Optionality works by negative information, reducing the space of what we do by knowledge of what does not work. For that we need to pay for negative results. (It is much easier to learn what is false than what is true, as Gurdjieff has said).

Some of the critics of these ideas —over the past two decades— have been countering that this proposal resembles buying "lottery tickets". Lottery tickets are patently overpriced, reflecting the "long shot bias" by which agents, according to economists, overpay for long odds. This comparison, it turns out is fallacious, as the effect of the long shot bias is limited to artificial setups: lotteries are sterilized randomness, constructed and sold by humans, and have a known upper bound. This author calls such a problem the "ludic fallacy". Research has explosive payoffs, with unknown upper bound —a "free option", literally. And we have evidence (from the performance of banks) that in the real world, betting against long shots does not pay, which makes research a form of reverse-bankingviii .

I don't want to be a party pooper but I feel tiny resentment when I hear about rich people make experiments getting into working class to have a trip out of their comfort zone and make a funny show about it. I know it's because I work as a postman, looking like a moron on a bike without brakes, I spent 6 hours on a hail and then a bilzzard on wednesday and I'm not gonna get an aword for that or I expect one") .

.

Please help me get over my bitterness. If I could change one thing this would be it. I was in a million embarrassing things, you've read my comments, it's embarrassing , I can teach you how to master it if you want.

, I can teach you how to master it if you want.")

.Please help me get over my bitterness. If I could change one thing this would be it. I was in a million embarrassing things, you've read my comments, it's embarrassing

, I can teach you how to master it if you want.Breo

The Living Force

I don't want to be a party pooper but I feel tiny resentment when I hear about rich people make experiments getting into working class to have a trip out of their comfort zone and make a funny show about it. I know it's because I work as a postman, looking like a moron on a bike without brakes, I spent 6 hours on a hail and then a bilzzard on wednesday and I'm not gonna get an aword for that or I expect one

Hi Martina, I am sorry you had such a terrible weather while doing your job. Thats demanding enough. But that your bike does not have brakes is just too dangerous. What stops you from fixing that asap?!

Please help me get over my bitterness. If I could change one thing this would be it. I was in a million embarrassing things, you've read my comments, it's embarrassing

I have not read all your comments, so I don´t know where your bitterness comes from. You might want to tell more about it.

If I look at myself in periods of frustration, I observe that then I do not dare to act in a way that I somehow know I should, could or long for. For me the lesson or message in the above interview is that this young man found his way to deal with rejection by taking the bull by its horns. It seems he succeeded and started his business on this topic. If not he could (have chosen to) become bitter.

Laura put the essence of it together like a condensed manual of action and observation:

What is most interesting is something we have discussed about many aspects of personality: that you can inoculate yourself against your triggers by deliberately exposing yourself to them! And, once the "triggering" stops being so automatic and powerful, your brain starts to come back online and you can actually work through the issues.

This is really helpful to let it sink in. To understand that once I start exposing myself deliberately to my triggers, their grip lessens. I then don´t have to loose myself in the many "why´s" but can focus on the how´s. And then the brain starts working again in a meaningful way. That´s a powerful guideline, IMO.

And there is also a great MindMatters show about Nassim Talib´s book, Anti-Fragility that Whitecost mentions:

"Antifragile is the property of things that gain from disorder: like muscle, economies, creativity, and character."

(Brakes for your bike, Martina

)I don't want to be a party pooper but I feel tiny resentment when I hear about rich people make experiments getting into working class to have a trip out of their comfort zone and make a funny show about it. I know it's because I work as a postman, looking like a moron on a bike without brakes, I spent 6 hours on a hail and then a bilzzard on wednesday and I'm not gonna get an aword for that or I expect one

Please help me get over my bitterness. If I could change one thing this would be it. I was in a million embarrassing things, you've read my comments, it's embarrassing

Hey Martina, I would say to simply try to appreciate the lesson or insight this person is trying to share as a human being, one who just happens to have a life context of being an entrepreneur or 'succesful' person, but whose insight can apply to anybody's life circumstances. For the matter, this forum isn't really aimed at entrepreneur-types - yet we can all absorb such lessons and use them to be better people.

Think about the book 'The 7 Habits of Highly Effective People' by Stephen Covey (discussed here). The tone is most of the times 'entrepreneurial', yet there are lots of lessons that can be applied to many areas of life. In fact, it is in that book that Covey mentions that if you want to expand, you should start with whatever is around, in your own area of influence and the things at your disposal. For those of us who don't own companies or get a spot on stage at a TED talk, we can still expand within our own jobs/families/relationships/life circumstances, etc. And I don't mean expanding economically or ascending the social ladder either. We weren't all meant to be rich - there are plenty of interesting lifes to be lived full of meaning other than the 'succesful' ones, so it's a bit of a waste of energy and time to be bitter at those people.

Do take care when riding a bike under a blizzard, and like Breo says, fix those breaks!

Trending content

-

-

Thread 'Coronavirus Pandemic: Apocalypse Now! Or exaggerated scare story?'

- wanderingthomas

Replies: 30K -